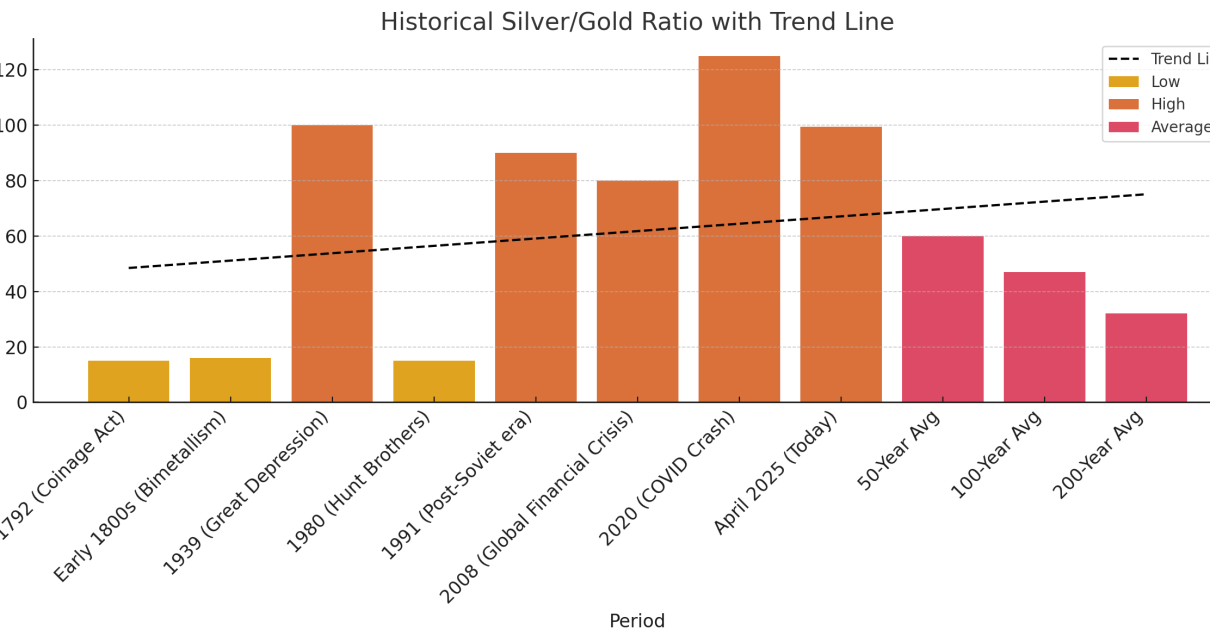

By Sean Dempsey, 04/15/25 The silver mining sector stands at the threshold of a potentially historic rally, driven by a rare confluence of macroeconomic imbalances, collapsing input costs, and structural mispricing. As of April 2025, the silver-to-gold ratio sits just under 100:1, a level that, while not unprecedented, remains among the most extreme in modern […]