by Sean Dempsey | 06/02/24

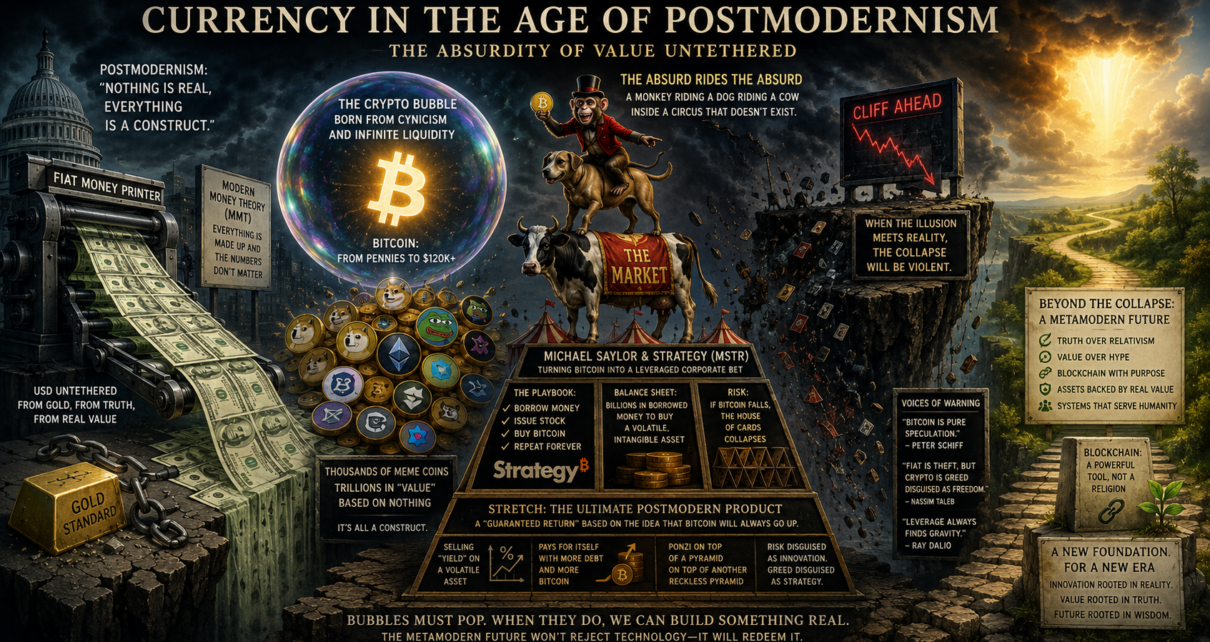

When I try to make sense of currency in the digital age, I start from a conviction that feels almost embarrassingly old-fashioned: money cannot survive without hard grounding; it must not subsist as mere style. It can be abstract, electronic, contractual, or symbolic, but it cannot be only mood. Philosophers of money have long noted that money is not exhausted by metal in the hand; it is also a social institution, a unit of account, a medium of exchange, and a store of value embedded in law, politics, and moral expectations. The BIS now describes money as a social convention sustained by the expectation that what is accepted today will be accepted tomorrow, while the Stanford Encyclopedia frames modern money debates as disputes over what money really is in metaphysical, political, and ethical terms. In other words, even before I get to crypto, I have to admit something many hard-money polemicists resist: money has never been only a shiny object. It is also trust, law, infrastructure, and a commonly recognized accounting language.

That is exactly why the postmodern turn matters to me. The Stanford Encyclopedia describes postmodernism as a family of practices that destabilize identity, certainty, historical progress, and singular meaning, while the Internet Encyclopedia of Philosophy emphasizes Lyotard’s skepticism toward metanarratives and his analysis of knowledge in computerized societies, where knowledge becomes externalized, commodified, and exchanged in quantifiable units. Lyotard’s language is not monetary policy, but I cannot shake the family resemblance: once a culture becomes habituated to treating meaning as circulation, signs as self-referential, and legitimacy as contingent, it becomes easier to imagine value itself as a floating text, endlessly repriced and narrativized. That does not prove a causal chain from French theory to bitcoin tickers. It does, however, describe the atmosphere in which financial abstractions feel normal, even glamorous.

Still, I do not think seriousness allows me to say the U.S. dollar is “nothing.” The gold link under Bretton Woods was real: foreign governments could convert dollars into gold at $35 an ounce, and Nixon’s August 1971 closure of the gold window effectively transformed the international system into a fiat one. Britannica is equally clear that fiat money is legal-tender money not redeemable in gold or silver. But the end of gold convertibility did not abolish reality; it shifted the anchor. The anchor became state credibility, tax capacity, central-bank settlement, and the institutional “singleness” of money. So when I say the dollar is untethered from hard metal, I mean exactly that. I do not mean that it is untethered from law, taxation, force, or institutional trust. Untethered from gold is not the same as untethered from everything.

That distinction is only important because it sharpens my real complaint. My complaint is not that modern money is symbolic. It always was, at least in part. My complaint is that the digital age has radicalized symbolism into spectacle. The postmodern mood does not create money out of thin air; rather, it encourages me to forget the difference between a symbol backed by institutional force and a symbol backed mostly by momentum, branding, and the next buyer. That forgetting, to my mind, is where our present disorder begins.

MMT is Economic Postmodernism on Steroids

If I am being honest, Modern Monetary Theory strikes me as the economic style-guide for a postmodern age. MMT proponents argue that a sovereign issuer of a non-convertible currency does not face a conventional budget constraint, cannot “run out of money,” and is constrained primarily by real resources and inflation rather than by financing in the household sense. Levy Institute summaries and Randall Wray’s work present this as a theory of sovereign currency grounded in chartalism: taxes and other obligations help drive demand for the state’s money, and the state determines the money of account. I understand the descriptive power of that framework. A government that issues liabilities everyone needs for taxes is plainly not a household.

But this is also where my skepticism hardens. To my ear, MMT often sounds like a world in which money becomes an editable legal text and fiscal limits become rhetorical rather than moral. The Banque de France’s critique is especially valuable here because it reminds me that, historically, MMT is not literally “born from postmodernism.” Its intellectual pedigree runs through Knapp’s State Theory of Money and Lerner’s functional finance, not through Lyotard or Baudrillard. The same paper argues that MMT turns money into a state-created token or representation, downplays the role of monetary-policy credibility, and ends up looking more like a political manifesto than a genuine theory. Gregory Mankiw, from a different tradition, likewise concludes that MMT contains some kernels of truth but that its most novel prescriptions do not follow cogently from its premises. Those are not my words; they are the words of serious critics across very different camps.

So I have to make a distinction that deep research forces on me. Historically, MMT is not a child of postmodern philosophy. But culturally, I still think it fits a postmodern sensibility. Why? Because it habituates the public to an unsettling idea: that money is not primarily an object but an authorized sign; not primarily a thing earned before spending, but a sovereign accounting tool; not primarily scarce in the old metallic sense, but institutionally managed and politically interpreted. Wray himself explicitly contrasts chartalist and “metalist” visions of money, and he notes that money can be regarded as a creature of law linked to contracts and obligations rather than to precious metal. That may be analytically defensible. It also, in my view, loosens the public imagination from older intuitions about discipline, constraint, and permanence.

I therefore do not want to caricature MMT as “nothing is real.” MMT scholars are very clear that inflation is real, resource bottlenecks are real, unemployment is real, and productive capacity is real. Their argument is about state finance under fiat conditions, not nihilism. But in a culture already trained to treat narratives as negotiable and symbols as sovereign, MMT can easily be received not as a careful theory of state money, but as a permission structure for the belief that value itself is infinitely scriptable. That reception matters politically even if it is not faithful to the best MMT scholarship.

Bitcoin in the Postmodern Age

Bitcoin is where I feel the postmodern atmosphere turn incandescent. Satoshi Nakamoto’s 2008 white paper did not describe bitcoin as a collectible, a treasury reserve, or a speculative macro instrument. It described “a purely peer-to-peer version of electronic cash” that would allow payments without a financial intermediary. Yet in practice bitcoin is treated in the United States as property for federal tax purposes, not as currency, and major central-bank and academic analyses still emphasize that its volatility undermines its usefulness as a unit of account and medium of exchange. One 2025 study concludes that bitcoin is better understood today as an investment asset than as a currency. To me, that is already a philosophical drama: the thing born as cash has become an asset; the thing marketed as money is often lived as speculation.

The price history is part of why the symbol became so culturally powerful. Bitcoin traded for pennies in its early life; it reached $1 in 2011, and by October 6, 2025 Coinbase recorded an all-time high of $126,210.50, while Reuters reported prices above $125,000 in early October 2025. As of the date of this article, June 2, 2026, the value of bitcoin is around $67,191. This arc tells me that bitcoin can be experienced less as currency than as a massive, globally shared referendum on narrative, scarcity, fear, and liquidity.

Nor did that ascent happen in a vacuum. The dollar’s gold convertibility had been gone for decades, pandemic-era money growth was historically abnormal, and by April 2026 M2 stood at $22.8 trillion after having grown at record rates during the COVID era. At the same time, Reuters tied bitcoin’s 2025 records to institutional demand, friendlier U.S. policy, ETF inflows, and a growing connection between bitcoin and global financial systems. So I can make the skeptical case that bitcoin benefited from an age of monetary looseness and distrust in legacy anchors, but I cannot honestly reduce the move to “the Fed printed and therefore bitcoin mooned.” The move was also institutional, regulatory, and cultural. It was a convergence of liquidity, access, legitimacy, and story.

Where the postmodern quality really reveals itself to me is in the way bitcoin is priced in dollars. I see one abstraction quoted in another abstraction, one floating signifier measured by another sign-system whose credibility rests on institutions rather than metal. Again, I do not mean “there is no reality underneath.” Bitcoin has protocol-enforced scarcity; the dollar has tax backing, central-bank settlement, and state power. But in everyday life what the public often experiences is not those foundations. They experience the screen. They experience the number. They experience the price line. In postmodern terms, the representation becomes more socially real than the underlying mechanism. That is why bitcoin feels, to me, like hyperreal money.

The meme-coin and “shit-coin” explosion only intensifies that feeling. In 2025, SEC staff described meme coins as cryptoassets inspired by memes, current events, characters, or trends, noted their speculative nature and significant volatility, and stated that holders are not protected by federal securities laws. The SEC further emphasized that the value of meme coins, in the cases it described, is derived from speculative trading and collective sentiment rather than claims on business income or managerial enterprise. That is as close to a regulatory description of postmodern finance as I am likely to get: sentiment, collectibility, volatility, entertainment, and no underlying claim on productive cash flow. So yes, I understand the rhetorical force of calling crypto-in-USD the poster child of postmodernism. I would state it slightly more carefully. I would say that crypto, especially when quoted in USD, dramatizes a culture in which symbols circulate faster than institutions can explain them, in which scarcity can be digital, legitimacy can be memetic, and wealth can be socially recognized long before it is economically grounded. That does not make all crypto worthless. It does mean the age has become dangerously comfortable with treating price as proof.

Saylor’s MicroStrategy and the Bubble Grows

For me, the spectacle becomes almost operatic when I get to MicroStrategy, now rebranded simply as Strategy. This is a bit of an ironic relabeling to my mind, as the company is not strategic in the least, but entirely speculative and tactical in its amoral product deployment. Nevertheless, in February 2025 the company announced that it was now doing business as Strategy, describing itself as the world’s first and largest Bitcoin Treasury Company while also still presenting itself as a large publicly traded business-intelligence and AI analytics firm. So I cannot responsibly call it a literal shell company. Formally and operationally, it still has a software business. But I also cannot ignore the obvious: the company itself says it adopted bitcoin as its primary treasury reserve asset and uses proceeds from equity and debt financings to accumulate bitcoin and offer investors varying degrees of economic exposure to bitcoin through equity and fixed-income instruments. In spirit, then, I regard it as shell-like: not because nothing is there, but because the bitcoin superstructure has grown so large that it increasingly defines what the market thinks the company is.

Strategy’s own quarterly filing states that it funds bitcoin purchases primarily from offerings of class A common stock and preferred stock, that it has also used convertible notes and secured borrowings, and that it may incur additional indebtedness in the future for the purpose of purchasing bitcoin. In the first quarter of 2026 alone, it sold 20.7 million shares of STRC, 33.5 million shares of common stock, and smaller amounts of STRK, taking in about $7.36 billion in total net proceeds. As of March 31, 2026, it still had enormous additional issuance capacity remaining under its at-the-market programs, including roughly $22.7 billion of STRC capacity and $27.2 billion of common-stock capacity. I do not have to exaggerate the machine; the machine is already extraordinary on its own terms.

Strategy also tells me, in language that is startlingly candid, that its liquidity needs include preferred-stock dividends, debt service, and other corporate obligations, and that it expects to meet those needs through some combination of USD reserves, bitcoin sales, securities sales under its ATM programs, and additional financings. It established a USD Reserve in December 2025 intended to support preferred dividends and debt interest, but the same filing makes clear that this reserve is not segregated, is not contractually locked for that purpose, and can be increased, reduced, or reallocated at management’s discretion. That matters because it means the structure is not anchored to a fenced cash pool. It is anchored to discretion, market access, and the ongoing ability to refinance or reprice belief.

The company’s own marketing language tells the story more vividly than any critic could. In a May 2026 free-writing prospectus, Strategy described its balance sheet as a “Digital Fortress” and said, without euphemism, “We Structure and Securitize Bitcoin.” Its cited balance-sheet slide showed about $15.5 billion of preferred equity and $8.2 billion of convertible debt against a bitcoin reserve around $67 billion. In another STRC roadshow document, Michael Saylor explained that the company expected bitcoin performance to support these instruments and noted that Strategy had issued $35 billion of securities over the prior year. When a company markets itself as a bridge to the “crypto economy” and openly frames itself as structuring and securitizing bitcoin, I think I am entitled to say that this is no longer mere treasury management. It is the industrialization of reflexivity.

I therefore see Strategy as the point where postmodern finance stops pretending to be embarrassed about itself. A protocol asset created as peer-to-peer cash gets absorbed into corporate treasury strategy. A public company then issues multiple layers of securities to warehouse more of that protocol asset. Those securities are then sorted into volatility bands and yield profiles so investors can buy custom slices of bitcoin exposure without directly owning bitcoin. If Baudrillard had wanted a case study in signs breeding signs, he could hardly have asked for a cleaner exhibit. That is my interpretation, not a formal theorem. But I do not think it is an unreasonable one.

The Recursive Pyramid of ‘Stretch’

Now, after perhaps too much bluster, I come to the incredible financial product I most wanted to scrutinize: Stretch, stock ticker STRC. Official materials claim that STRC does not offer a guaranteed return. Strategy’s own website says STRC is perpetual preferred stock that currently pays an 11.50% annual dividend, payable monthly in cash, with the rate adjusted monthly to encourage trading near a $100 par value. The same page explicitly warns that the current rate is not indicative of future rates, that the rate may be significantly lower, and that the cash dividend is not guaranteed. The prospectus supplement is even clearer: regular dividends are payable only “when, as and if declared” by the board; the certificate does not require the company to declare them even if funds are legally available. That matters enormously. However theatrical my skepticism becomes, I cannot honestly describe STRC as a contractual guarantee.

What STRC is, rather, is an unusually engineered layer of credit-like exposure issued by a company whose fundamental economic identity is increasingly tied to bitcoin. The July 2025 prospectus set the product up at a $100 stated amount, with an initial 9.00% dividend rate, adjustable monthly by management. Strategy’s stated intention was to use those rate adjustments to keep STRC trading at or near $100. The prospectus also provided for cash redemption at $101 or more, compounded dividends if declared dividends go unpaid, and a liquidation-preference framework that can ratchet depending on trading prices and new issuance activity. In plain English, this is not a sleepy old preferred share. It is a managed instrument designed to behave like short-duration, high-yield credit while living inside a bitcoin-heavy capital structure.

That design is precisely why I find it unnerving. Strategy’s filings warn that it may not have sufficient cash to pay dividends, that contractual restrictions may limit its ability to do so, and that the board may simply choose not to pay accumulated dividends on STRC. The company has also said outright that bitcoin does not generate interest or other returns, so the ability to earn from bitcoin depends on appreciation. In its 2025 STRC prospectus, Strategy acknowledged that bitcoin had traded below $50,000 and above $120,000 in the preceding year; in other words, the issuer itself reminds buyers that its underlying macro substrate is violently unstable. To me, that turns the product into a kind of recursive wager: income is being packaged on top of an asset that does not itself throw off income, by an issuer that often replenishes liquidity through yet more securities issuance.

And in 2026 the recursion got more literal. Strategy’s March 2026 quarter showed $229.5 million of cash dividends paid across its preferred-stock complex in the quarter alone. By May 3, 2026, the company said cumulative dividends declared and paid on preferred stock had reached $692.5 million. On June 1, 2026, Strategy disclosed that it had sold 32 bitcoin for $2.5 million and that the proceeds were expected to fund distributions on preferred stock. That sale was symbolically tiny against more than 843,000 bitcoin holdings, but it was philosophically huge: the machine that had spent years preaching “never sell” had, in fact, sold bitcoin to service the overlay of yield products built atop the bitcoin hoard. That is the moment where, for me, the monkey is no longer just riding the dog; the dog has begun selling bits of the circus tent to keep the acrobats paid.

I want to be extremely careful with language here. Legally I cannot, at least on the present evidence, call STRC or Strategy a legal Ponzi scheme. A Ponzi technically requires fraud of a specific kind, and the company’s filings are conspicuous in disclosing risks, optionality, and the non-guaranteed nature of dividends. But I can say that I regard the structure as pyramid-like in an economic and philosophical sense. It depends heavily on fresh demand for securities, continued market confidence in bitcoin, management’s ability to maintain trading optics, and the possibility of using common equity, preferred equity, reserve cash, or bitcoin sales to keep obligations serviced. Strategy itself admits that it may use proceeds from additional securities sales or bitcoin sales to fund liquidity needs, including preferred dividends. That is not a courtroom accusation. It is a balance-sheet observation.

Steel-maning the Counter-Argument

The strongest rebuttal to my skepticism is not stupid, and I do not want to pretend it is. BlackRock’s 2025 paper argues that bitcoin’s risk and return drivers are meaningfully different from those of traditional assets, that some investors view it as a scarce, non-sovereign, decentralized global asset, and that adoption could be driven by monetary instability, geopolitical instability, and fiscal concerns. State Street similarly argues that institutions increasingly see bitcoin not merely as a speculative detour but as a strategic allocation, with diversification benefits, improving regulatory clarity, and a role as a debasement hedge. Even Lyn Alden, who is more crypto-native than BlackRock, makes a serious structural argument that corporate bitcoin treasury strategies and bitcoin-related securities can channel capital with mandates into the asset class and broaden access. I may dislike the age, but I do not get to wave away the fact that some of the world’s largest allocators now view bitcoin as a legitimate portfolio input.

There is also a more charitable reading of Strategy than the one I instinctively prefer. On that reading, Strategy is not a circus but a financial intermediary translating bitcoin exposure into forms different investors can tolerate. Some want raw bitcoin volatility; some want amplified equity; some want convertible exposure; some want preferred dividends with lower volatility. Strategy’s own roadshow says STRC targets “low volatility, short duration, high-yield credit,” and its materials repeatedly emphasize optionality across equity, credit, and capital instruments. One might say this is not madness at all, but market completion: a new commodity-money-adjacent asset class generating its own stack of wrappers, much as mortgages, commodities, and sovereign debt generated layers of securities before it.

There is even a deeper counterargument, one I have to respect because it cuts beneath price. Bitcoin, unlike meme coins, does have a hard supply cap of 21 million. Unlike many promotional tokens, it was introduced as an open, decentralized protocol, and its historical significance in digital monetary design is undeniable. If I am fair, I have to admit that bitcoin is not merely “nothing”; it is code, consensus, network security, and an operating monetary experiment that has survived for more than a decade and a half. And unlike pure joke tokens, it has become embedded in ETFs, treasury strategies, custody systems, derivatives markets, and even geopolitical policy debates. That does not prove the valuations are sane. It does prove the phenomenon is no longer dismissible as a toy.

Still, the same official materials that make the bullish case also qualify it. BlackRock itself says bitcoin is high-risk on a standalone basis and that investment can entail total loss. State Street’s institutional-bullish case still hinges on maturation, regulation, and portfolio theory rather than on bitcoin functioning as everyday money. And Strategy’s own filings repeatedly warn that its bitcoin holdings heavily affect its financial results and the market price of its listed securities, that unrealized gains do not generate cash, and that it may need to sell bitcoin if reserves and financing are insufficient. So even the best case for the other side is not “this is now safe and solid.” The strongest honest case is, rather, “this is risky, novel, increasingly institutional, and perhaps structurally important.” I can grant that sentence without surrendering my skepticism.

Metamodern Synthesis: What Comes After Postmodern Currency?

My optimism begins exactly where my skepticism peaks. I do not think the answer is to deny digitality, deny programmability, deny tokenization, or pretend that blockchain never solved anything. OECD work on tokenization emphasizes genuine potential benefits: automation, lower transaction costs, faster clearing and settlement, transparency, fractionalization, improved liquidity for previously illiquid assets, and programmable post-trade functionality. The BIS has likewise argued that tokenized financial systems can create new possibilities, especially when paired with trusted settlement assets. The FCA and Bank of England in May 2026 explicitly set out a shared vision for tokenization in UK wholesale markets. So when I say I want the bubble to pop, I am not saying I want the technology buried with it. Quite the opposite. I want the technology rescued from the hype cycle that has so often disfigured it.

I think this is where the metamodern philosophy matters to me. The literature on metamodernism describes it as oscillating between modern hope and postmodern irony, or as a stance of informed naivety and pragmatic idealism. That language is useful precisely because it does not require me to become gullible again. It does not ask me to forget the failures of grand narratives, speculative fever, and ideological certainty. But it also refuses to remain trapped in pure cynicism. For finance, that would mean retaining postmodern suspicion toward hype, spectacle, and self-referential narratives while recovering a modern appetite for building institutions, standards, and durable value. That is the future I actually want.

So my closing hope is not that digital assets disappear. My hope is that the age of confusion between investing and speculating eventually breaks. Bubbles do pop, even when they are narrated as civilizational destiny. When they do, I suspect the useful residue will be obvious. Open ledgers will still matter. Tokenized claims on real assets will still matter. Programmable settlement and auditable records will still matter. What I hope gets left by the roadside is the endless recursion in which a volatile asset is wrapped in corporate leverage, wrapped in preferred structures, wrapped in marketing rhetoric, wrapped in social-media certainty, and then sold back to the public as a new species of prudence. A metamodern future for blockchain would, in my view, be one where digital rails remain, but valuations reconnect to productive use, legal clarity, real collateral, and hard-earned trust.

Open Questions Remain

My central thesis here is partly interpretive. I can document what postmodernism says, what MMT says, how fiat money works after 1971, how bitcoin prices evolved, and how Strategy’s securities are structured. But my claim that our current monetary moment epitomizes postmodernism is ultimately my personal, philosophical reading of those facts, not necessarily a theorem any filing can prove. Likewise, while I think it is fair to describe Strategy’s architecture as recursively reliant on sentiment and market access, the official record does not precisely show a legal guarantee on STRC so time will tell if it rises to the moniker of Ponzi scheme. Finally, MMT is historically rooted more in chartalism and functional finance than in postmodern theory, even if I continue to think it resonates with a postmodern cultural mood.

References:

https://www.bis.org/publ/arpdf/ar2025e3.htm

https://plato.stanford.edu/entries/postmodernism

https://www.federalreservehistory.org/essays/gold-convertibility-ends

https://publications.banque-france.fr/sites/default/files/medias/documents/wp833_0.pdf

https://www.levyinstitute.org/pubs/wp_792.pdf

https://bitcoin.org/bitcoin.pdf?utm_source=chatgpt.com

https://www.coinbase.com/price/bitcoin

https://www.stlouisfed.org/on-the-economy/2023/may/the-rise-and-fall-of-m2

https://www.sec.gov/newsroom/speeches-statements/staff-statement-meme-coins

https://www.strategy.com/press/microstrategy-is-now-strategy_02-05-2025

https://www.sec.gov/Archives/edgar/data/1050446/000105044626000031/mstr-20260331.htm

https://www.sec.gov/Archives/edgar/data/1050446/000119312526237912/d101092dfwp.htm

https://www.strategy.com/strc/learn

https://www.sec.gov/Archives/edgar/data/1050446/000119312525165531/d852456d424b5.htm

https://www.blackrock.com/us/financial-professionals/insights/bitcoin-unique-diversifier

https://www.sec.gov/Archives/edgar/data/1050446/000119312525161953/d896883dfwp.htm